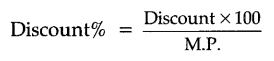

Discount is a reduction given on marked price.

Discount = Marked Price – Selling price.

Discount can be calculated when the discount percentage is given.

Discount = Discount % of marked Price.

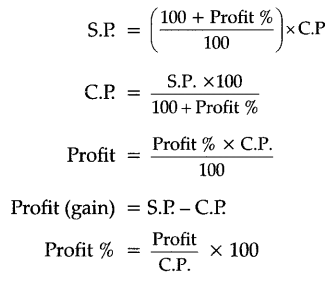

Additional expenses made after buying an article are included in the cost price and are known as overhead expenses.

C.P = Buying Price + Overhead expenses

Sales tax is charged on the sale of an item by the government and is added to the bill amount.

Sales tax = Tax % of bill amount

VAT (value added tax) is charged on the selling price of an article.

Percent: The word percent is an abbreviation of the Latin phrase ‘per centum’ which means per hundred or hundredths.

Simple Interest(SI): When the interest is paid to the lender regularly every year or half year on the same interest, we call it a simple interest. In other words, interest is said to simple, if it is calculated on the original principle throughout the loan period.

S.I.=P×R×T/100

Where, P = Principal, R = Rate of Interest, T = Time.

Compound Interest (CI): If the borrower and the lender agree to fix up a certain interval of time (say, a year or a half-year or a quarter of a year, etc.), so that the amount at the end of an interval becomes the principal for the next-interval, then the total interest over all the interval calculated in this way is called the compound interest.

Also, CI = Amount – Principal

(a) When interest is compounded annually, then

where P is Principal, R is the rate of interest and n is time period.

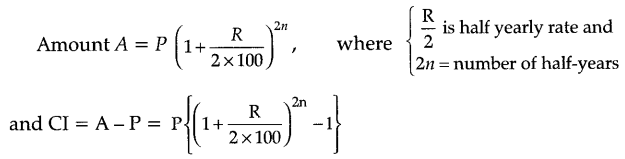

(b) When Interest is Compounded Half-Yearly, then

When R1, R2 and R3 are different rates for the first, second and third year, then